💊 Trend Isn’t Broken, But the Road Just Got Rougher

More Straight Talk on Pharmacy Risk from a Stop Loss Underwriter

We knew pricing trend wasn’t going to stay quiet forever. But in just the past few weeks, the noise got louder—from trade barriers to PBM antics to a supply chain held together with duct tape and hope. So here’s where we stand now, and what we’re watching hard as we head into renewal season.

🚧 Tariffs, Treaties, and a Messy Middle

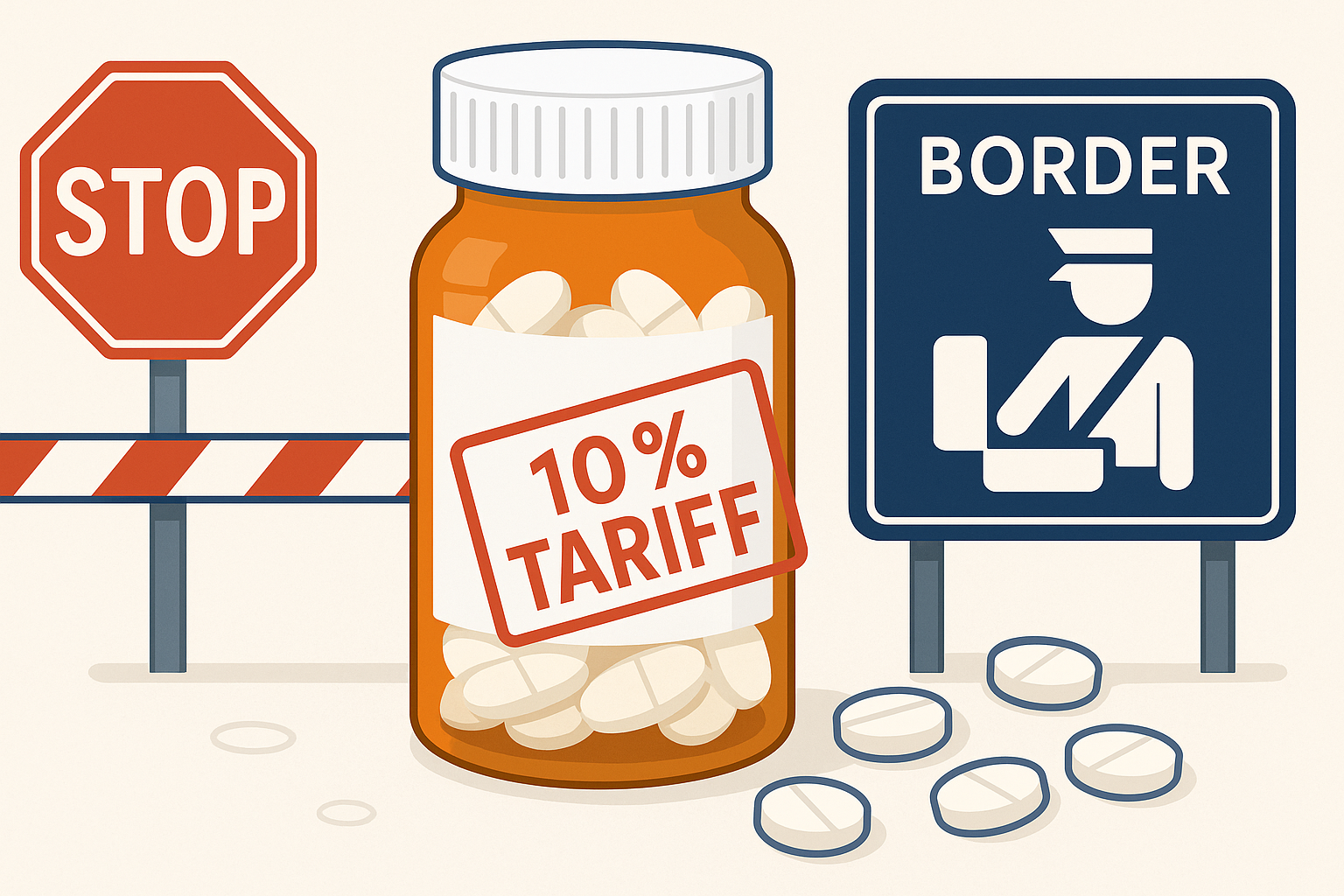

It’s confirmed: **APIs from China are effectively embargoed**, and **most pharmaceutical imports from Mexico and Canada are now subject to a 10% tariff**—unless they qualify under USMCA. That’s the catch. Some drugs will be exempt, but only if they meet strict country-of-origin rules and paperwork requirements. That’s not most of them.

Bottom line? We can’t assume Canadian or Mexican drugs stay cheap. And even for USMCA-qualified imports, the admin overhead alone could create delays or sourcing headaches. Pricing has to reflect that risk.

🔄 Supply Chain Snags Are Back

Drug shortages are stacking up again. Delayed shipments. Raw material scarcity. And now, even the mail system’s getting pulled into the drama.

USPS strike activity is brewing—not the whole Postal Service, but a major contractor that handles prescription shipments for national PBMs is striking across multiple states. If that expands? That’s a real delivery issue for patients who rely on home delivery. Cost aside, access is becoming a factor again.

🧪 Biosimilars Are a Battleground

We’re still watching the Humira effect—but here’s what’s changed: **PBMs are now private-labeling biosimilars**, slapping their own names on them, and then manipulating formularies to push those versions instead of the lowest-cost option.

It’s like buying the store brand but paying name-brand prices. The plan sponsor sees “biosimilar savings,” but the PBM is collecting the rebate stack, or expanding their margins in other ways. That’s not savings. That’s steering.

🧠 GLP-1s: From Obesity to Alzheimer’s?

Just when brokers started to wrap their heads around GLP-1s for weight loss, the use cases are expanding: Alzheimer’s, Parkinson’s, fatty liver, osteoarthritis, even alcohol addiction. That’s five new trend lines in the making.

Here’s the kicker—**the big carriers are still greenlighting GLP-1 coverage liberally**, while disciplined plans are capping it, carving it out, or leveraging MAP programs (what little bit they can these days). We’re seeing **12–13% pharmacy trend on the BUCA side** in 2025, and half that in groups with an intentional strategy. But these predictions were before the tariffs kicked in.

Silver lining: CMS has denied Medicare coverage for GLP-1s used purely for weight loss. That gives employers cover to rethink benefit inclusion—and gives you, the broker, air cover to say no to casual coverage. However, when Medicare heading down the path of negotiating price on select Medicare drugs, we can surely count on more cost shifting to the private sector. Its never easy! 😪

⚖️ So What’s Our Underwriting Play?

We’re not rubber-stamping trend or penalizing good strategy. Instead, we’re looking closely at:

- Whether a group’s pharmacy is integrated or carved out

- Whether their PBM plays games—or plays it straight

- If GLP-1s are included, and under what clinical guardrails

- What exposure they might have to tariff-linked sourcing

- Whether we can build a plan to make this a non-issue

Don’t let the noise get you down – get ahead of the conversation with your clients! We have strategies that can turn a 5-7% projected tariff increase into a net-zero impact by rethinking plan design and vendor alignment. If you’re a broker seeing red flags—or just want to get ahead of the curve—talk to us. We’re not just pricing for today. We’re helping you lead.

📞 Let’s schedule a call and talk through how we’re approaching this on renewals.