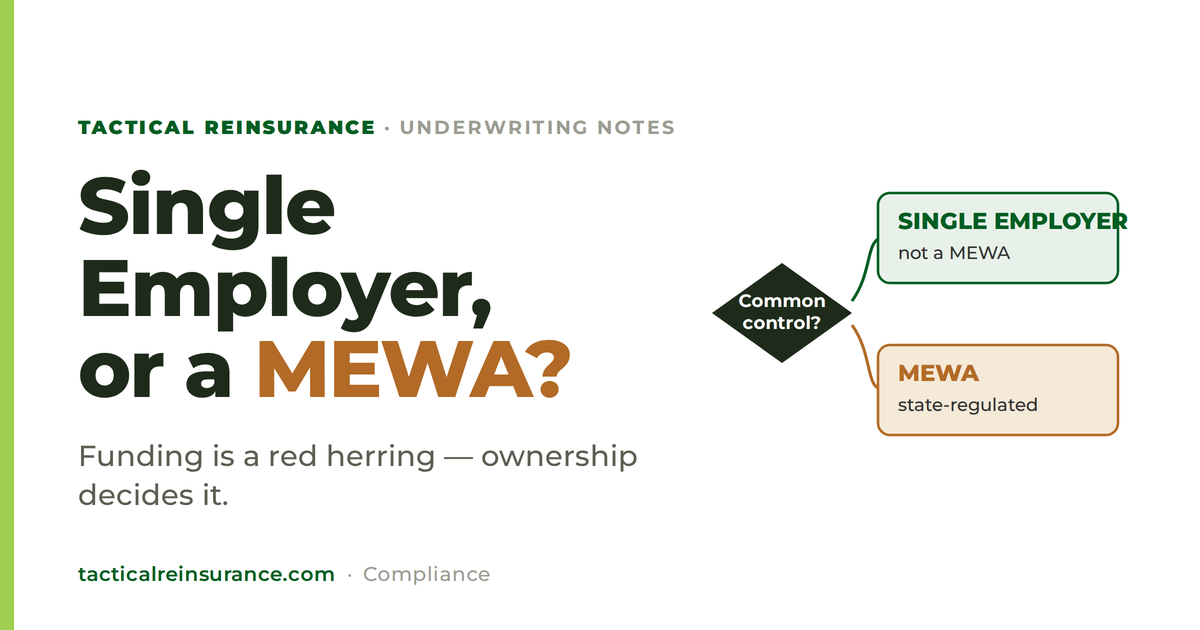

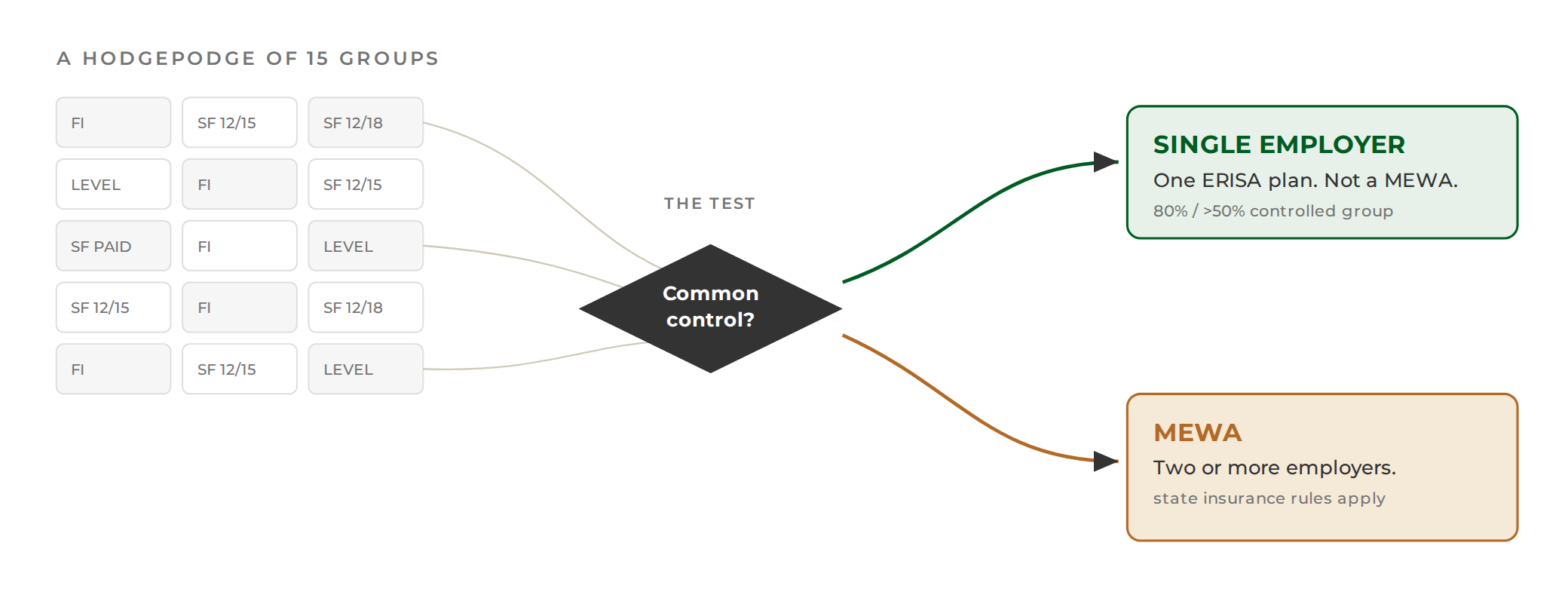

We just took in a block of fifteen employer groups. Some are fully insured, some are self-funded on 12/15 running contracts, a couple are on other bases — honestly, it’s a hodgepodge. And before we quote a dime of it, there’s one question we have to answer: are we looking at one employer here, or a whole bunch of them?

That sounds like a small distinction. It isn’t. The answer decides whether this is a plain single-employer health plan or a MEWA — a multiple employer welfare arrangement — and those two live under completely different rules.

Why this matters

A single-employer plan sits inside ERISA, and ERISA mostly keeps the states out of it. A MEWA doesn’t get that cover. When Congress wrote the MEWA rules back in 1983, it did it specifically so states could regulate these arrangements as insurance — so a MEWA is exposed to state licensing, reserve and solvency requirements, and MEWA registration, even when it’s self-funded. A lot of states flat-out won’t allow a self-funded MEWA. On top of that, a MEWA has to file a Form M-1 with the Department of Labor.

So this is not a labeling exercise. Call a MEWA a single-employer plan and you’ve got an unlicensed insurance operation in the eyes of the state. Treat a real single employer like a MEWA and you’ve buried a legitimate plan under rules it never had to follow.

Funding isn’t the question. Ownership is.

Here’s the part people trip on with a block like ours. Whether a group is fully insured, self-funded on a 12/15, a 12/18, a paid contract, level-funded — none of that tells you a thing about MEWA status. Funding is a financing decision. It doesn’t change who the employers are.

You can line up fifteen groups funded exactly the same way and still have a MEWA, or fifteen funded every which way and have a single employer. So the 12/15s and the fully insured cases in this block are a sideshow. The only thing that answers the question is ownership and control.

What “one employer” actually means

The law doesn’t care whether the groups feel related, use the same broker, or sit in the same association or captive. It asks one thing: are they a controlled group — are they under common control? And it answers that with hard ownership math, borrowed from the IRS controlled-group rules (IRC §1563, §414(c)) that ERISA §3(40) points to.

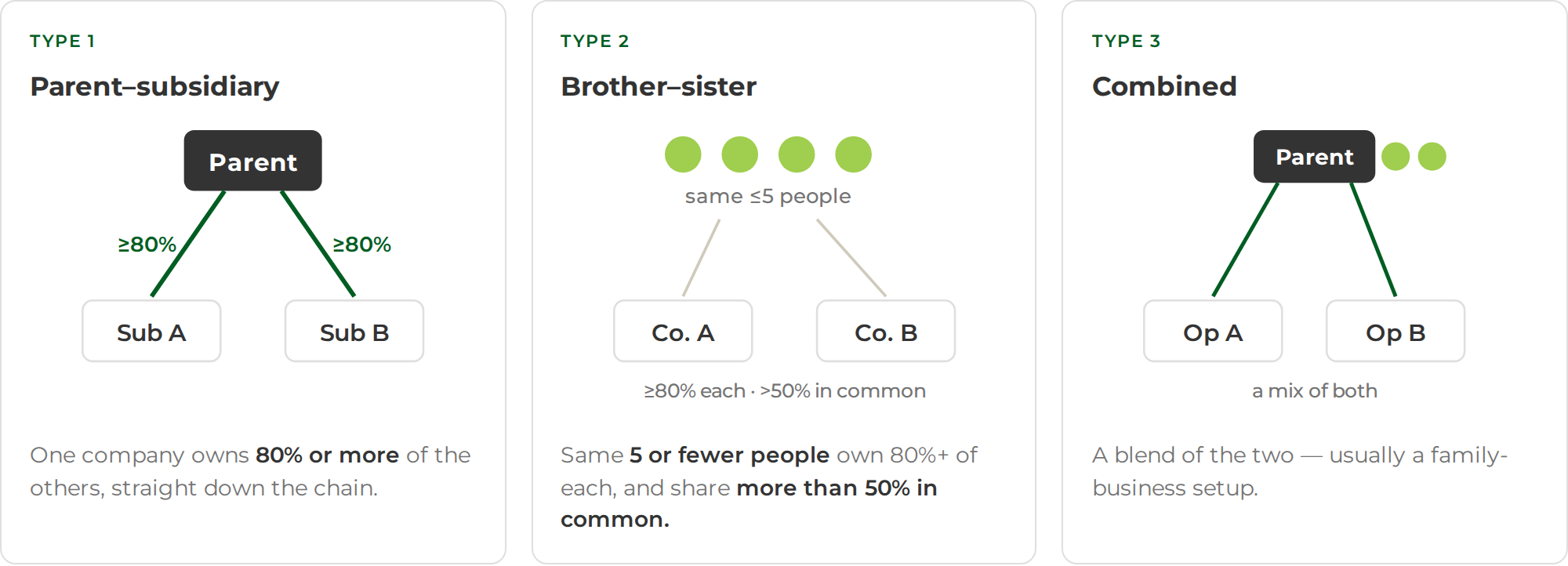

There are three ways to get there:

Parent-subsidiary. One company — the common parent — owns 80% or more of the others, straight down the chain.

Brother-sister. This one’s two separate hurdles, and you have to clear both.

First, the same five or fewer people have to own at least 80% of each company when you add up their stakes. That part’s straightforward.

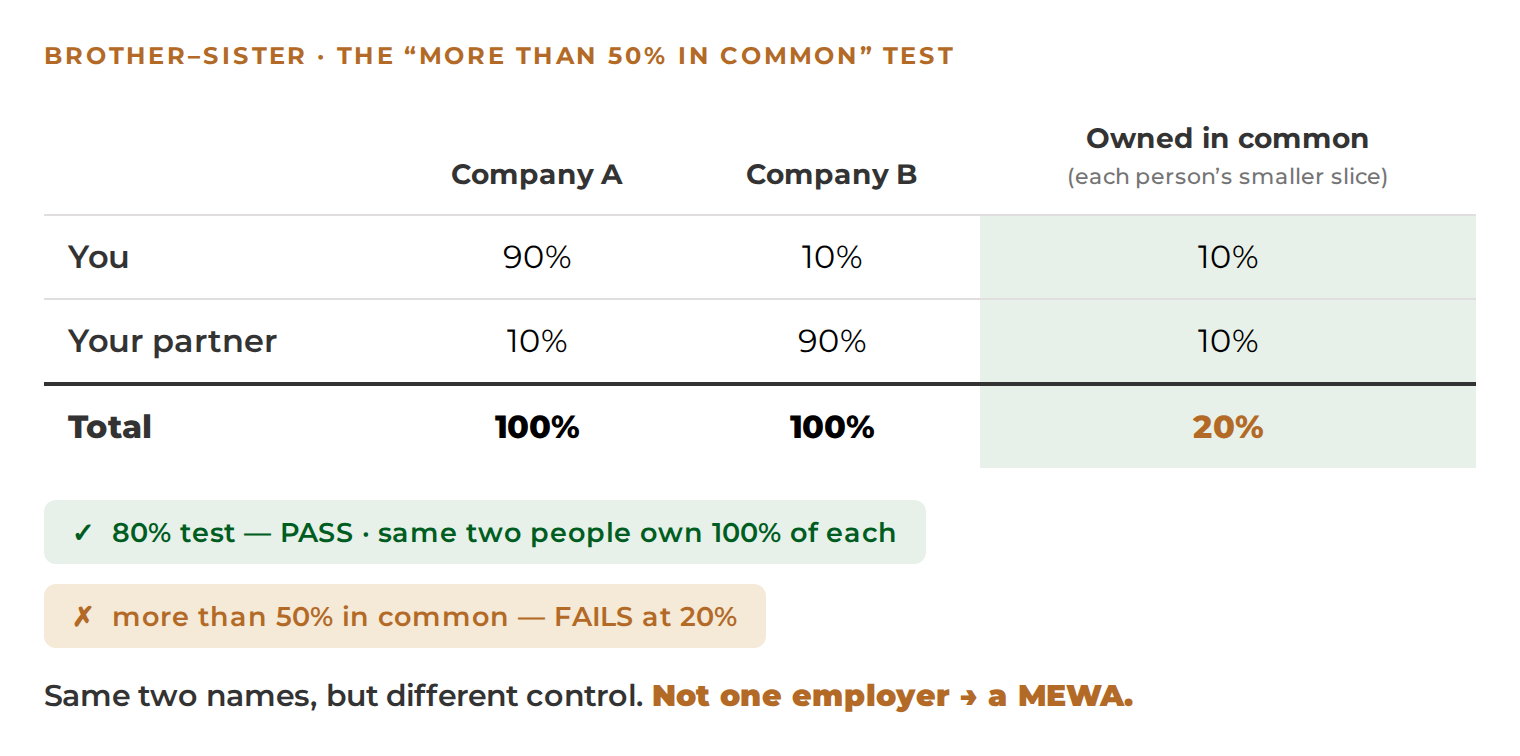

Second — and this is the one that trips people up — those same people have to share more than 50% in common across the companies. “In common” is the whole game. You don’t count each person’s full stake; you count only the piece they own in every company, which is their smallest slice. So somebody who owns 90% of one company but 10% of the other brings just 10% to this test, because 10% is all they own in both.

Why does that matter? Picture two people who together own 100% of two companies — but flipped: one owns 90% of the first and 10% of the second, the other owns it the other way around. They clear the 80% test easily. But their common ownership is only 20%, so they fail the 50% test, and they’re not a controlled group. Which is exactly right — one of them really runs the first company, the other really runs the second. Same two names, different control. That 50% test is what catches it.

Combined. A mix of the two, usually in a family-business setup.

Miss those thresholds and you’re not a single employer. You’re a MEWA.

The 25% thing — and why it’s mostly a distraction

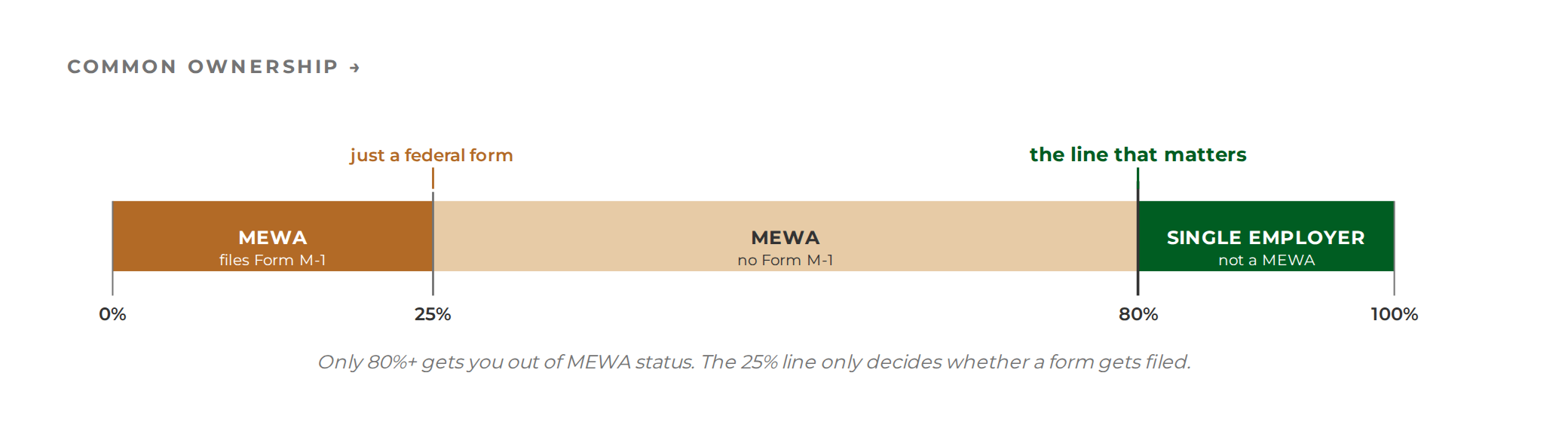

There’s a 25% number floating around in the MEWA rules, and it confuses everybody, so let me put it where it belongs.

That 25% is a reporting rule. If a plan covers businesses that share at least 25% common control, it doesn’t have to file the federal Form M-1. That’s the whole job it does. It is not the test for whether you’re a single employer — that’s still 80% / more-than-50%. The DOL has said as much: 25% is for the filing requirement, not the determination.

Which means the middle band — 25% to 80% — is exactly where people get a false sense of security. An arrangement sitting in there is still a MEWA. It’s still subject to state insurance regulation. It just doesn’t owe the DOL a form. “No M-1 required” is not “you’re in the clear.” So for us, the line that actually matters is 80%. Below that, we treat it as a MEWA and run the state analysis regardless of which side of 25% it lands on.

Has anybody ever softened these rules?

Fair question, and I went looking. Short answer: not really — if anything, the regulators and courts have leaned the other way.

The Supreme Court, back in Vogel Fertilizer, actually tightened the brother-sister test rather than loosening it (that’s where the “you have to own a piece of every company to count” rule comes from). And the DOL has swatted down attempts to game it. The clearest example: a PEO tried to manufacture single-employer status by taking options to buy 80% of each client company. The DOL wouldn’t give the options any weight without a real business reason beyond dodging state insurance law. The whole point of these rules was to stop promoters from hiding behind ERISA, so nobody’s in a hurry to hand out relief.

The one real crack cuts the other way, and it’s the 25% clause itself. Because the statute says common control “shall not be based on an interest of less than 25 percent,” at least one regulator — the New York Department of Financial Services — reasoned that Congress must have meant common control can be found below 80%, or that 25% language means nothing. On that logic, New York said a subsidiary owned somewhere between 50% and 80% isn’t automatically a MEWA. So there’s a live argument that 25%-to-80% common ownership gets you out of MEWA status. But it’s contested, it’s state-by-state, and it’s the employer’s counsel who’d have to stand behind it — not something we’d ever underwrite on.

How we screen a block like this

With fifteen groups in front of us, the question isn’t how they’re funded — it’s how they’re owned. We line the entities up and look for the ownership threads: a common parent, or the same handful of people showing up across the cap tables. Then we run those relationships against the tests above.

Most “hodgepodge” blocks that show up as an assembled book of unrelated employers — pulled together by an association, a marketing group, some kind of program — are going to land in MEWA territory, precisely because there’s no common ownership tying them together. A block that turns out to be one family’s operating companies, or a parent and its subs, goes the other way. The only way to know is to actually look at the ownership, group by group.

Bottom line

The funding mix is the puzzle everyone stares at. The employers are the answer. Whether this is a single-employer plan or a MEWA comes down to ownership and control — 80% is the line, the 25% is just about a federal form, and the people who actually know the cap tables are the ones who make the call.

Tactical Reinsurance provides this for general education. It isn’t legal, tax, or accounting advice, and reading it doesn’t make us your advisor. Controlled-group and MEWA determinations turn on facts only the employer and their tax professional can confirm — so talk to your own CPA, tax adviser, or ERISA counsel before you rely on any of it.